The case of Silicon Valley Bank

and what we can learn from it...

On March 12, 2023, the financial world was shaken by the sudden collapse of Silicon Valley Bank (SVB). It was a renowned institution that had been a fixture in the technology industry for decades.

Investors who had entrusted their money to SVB suddenly found themselves unable to access their funds. The reason: The bank was unable to meet its obligations due to a severe liquidity crisis and a bank run. A bank run occurs when many investors withdraw money from the bank simultaneously. For SVB, this was fatal in combination with the liquidity crisis – it had to file for bankruptcy.

1. Causes of the SVB Collapse: The Economic Context

To understand the causes of the SVB collapse, we need to consider the broader economic context in which it occurred. In recent years, the global economy has been driven primarily by three measures aimed at keeping the financial system running: massive credit expansion, low interest rate policies, and central bank asset purchase programs (quantitative easing).

This easy money has driven up asset prices and encouraged investors to take on more and more debt. This has led to a dangerous accumulation of leverage and risk.

2. What Happened at Silicon Valley Bank?

SVB was no exception to this trend. Like many banks, it had leveraged its balance sheet to maximize profits and expand its business. It had aggressively lent to technology start-ups, often with little regard for the prospects of these companies. As long as the tech boom continued, SVB seemed like a safe bet for investors.

However, when the Federal Reserve raised interest rates in response to rising inflation, the situation changed. As borrowing costs increased, many SVB customers could no longer service their debts. The tech bubble that had contributed so much to SVB's growth began to burst, and investors withdrew their funds. The bank faced a portfolio of risky, illiquid assets, primarily mortgage-backed securities and interest-bearing ten-year Treasury bonds, which could only be liquidated at a loss of $1.8 billion. Due to rising interest costs, the entire US banking sector saw unrealized gains (losses) on investment securities and losses on available-for-sale and held-to-maturity securities totaling $620 billion in the fourth quarter of 2022. This represents a decline of $69.5 billion from the previous quarter and reached the highest level since the financial crisis of 2007/2008.

3. Lehren aus dem Zusammenbruch der SVB

Der Zusammenbruch der SVB verdeutlicht, in welch großer Gefahr Volkswirtschaften schweben, die auf Verschuldung basieren. Außerdem zeigt er die Risiken von quantitativen Lockerungen. Wenn Kredite uneingeschränkt ausgeweitet werden dürfen, schafft dies ein falsches Gefühl des Wohlstands, das die Schwächen der Wirtschaft verschleiern kann. Wenn Gelder plötzlich zurückgezogen werden und Kredite ausfallen – wie im Fall der SVB – können die Folgen katastrophal sein.

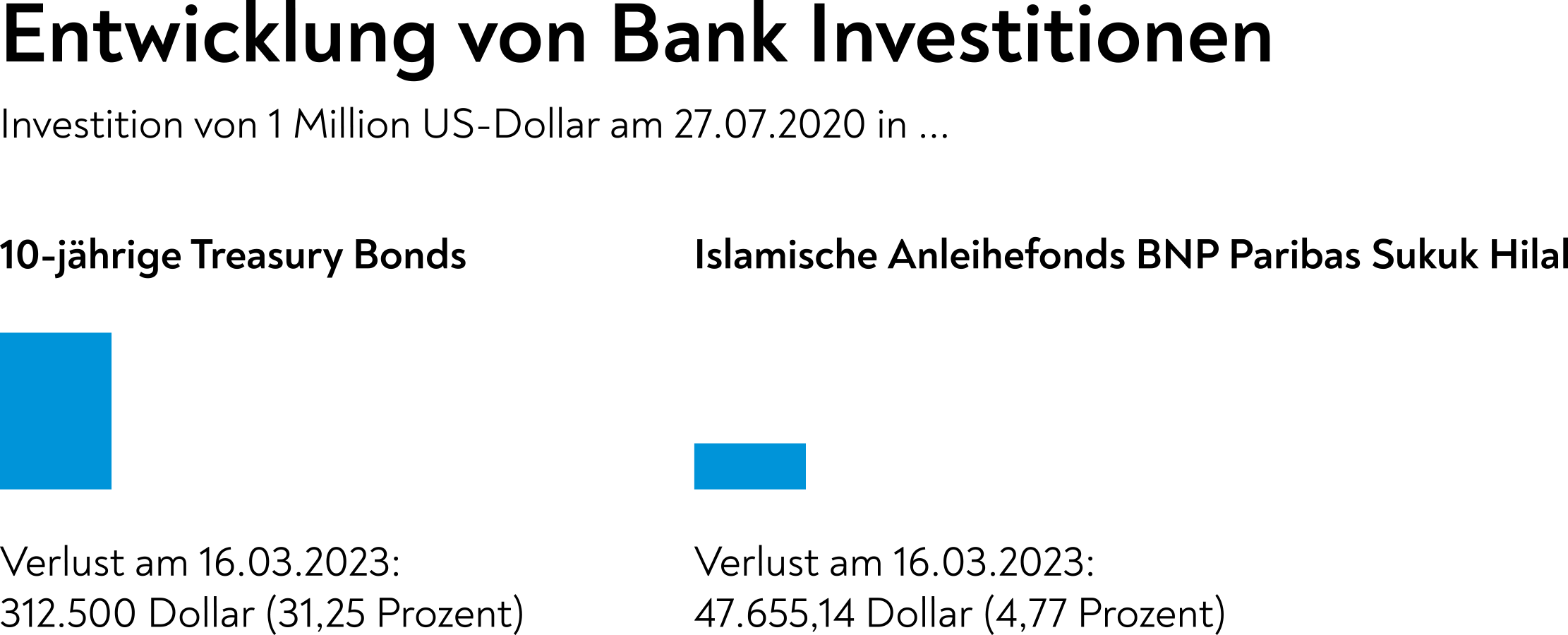

4. Investment in Ten-Year Treasury Bond vs. BNP Paribas Sukuk Hilal Islamic Bond Fund

On June 27, 2020, Bank A invested $1 million in a ten-year Treasury bond with an interest rate of 0.55%. The maturity date of this Treasury bond would be June 27, 2030. However, due to high central bank interest rates and a liquidity crunch, the bank had to liquidate the Treasury bond on March 16, 2023, at a new interest rate of 3.7%.

Formula: Loss = Principal x (New Interest Rate - Old Interest Rate) x Time

Where:

- Principal = $1,000,000

- New Interest Rate = 3.7%

- Old Interest Rate = 0.55%

- Time = Number of years until maturity

- Time = (Maturity Date - Purchase Date) / 365

- Time = (June 27, 2030 - June 27, 2020) / 365

- Time = 10 years

Using the above formula, we can calculate the loss:

Loss = $1,000,000 x (3.7% - 0.55%) x 10 = $312,500

Therefore, the bank would incur a loss of $312,500 or 31.25% of the initial investment. The bank's investment in the Treasury bond was exposed to interest rate risk, leading to a significant loss as interest rates rose.

Now, let's consider the second scenario. Suppose Bank B invested $1 million in the BNP Paribas Sukuk Hilal at a price of $1612.26 per certificate on June 27, 2020. The Sukuk Hilal is a type of Islamic bond structured in accordance with Sharia principles. The bank acquired a total of 619 certificates with an initial investment of $1 million. Assuming market conditions and a liquidity crunch forced the bank to sell the Sukuk Hilal certificates at a price of $1535.51 per certificate on March 16, 2023.

Formula: Gain/Loss = (Selling Price - Purchase Price) x Number of Certificates

Where:

- Purchase Price = $1612.26

- Selling Price = $1535.51

- Number of Certificates = $1,000,000 / $1612.26 = 619

Using the above formula, we can calculate the gain/loss:

Gain/Loss = ($1535.51 - $1612.26) x 619

Gain/Loss = -$47,655.14

Therefore, the bank would incur a loss of $47,655.14 or 4.77% of the initial investment. The bank's investment in the BNP Paribas Sukuk Hilal was exposed to market risk, leading to a much smaller loss compared to the same investment in a ten-year Treasury bond.